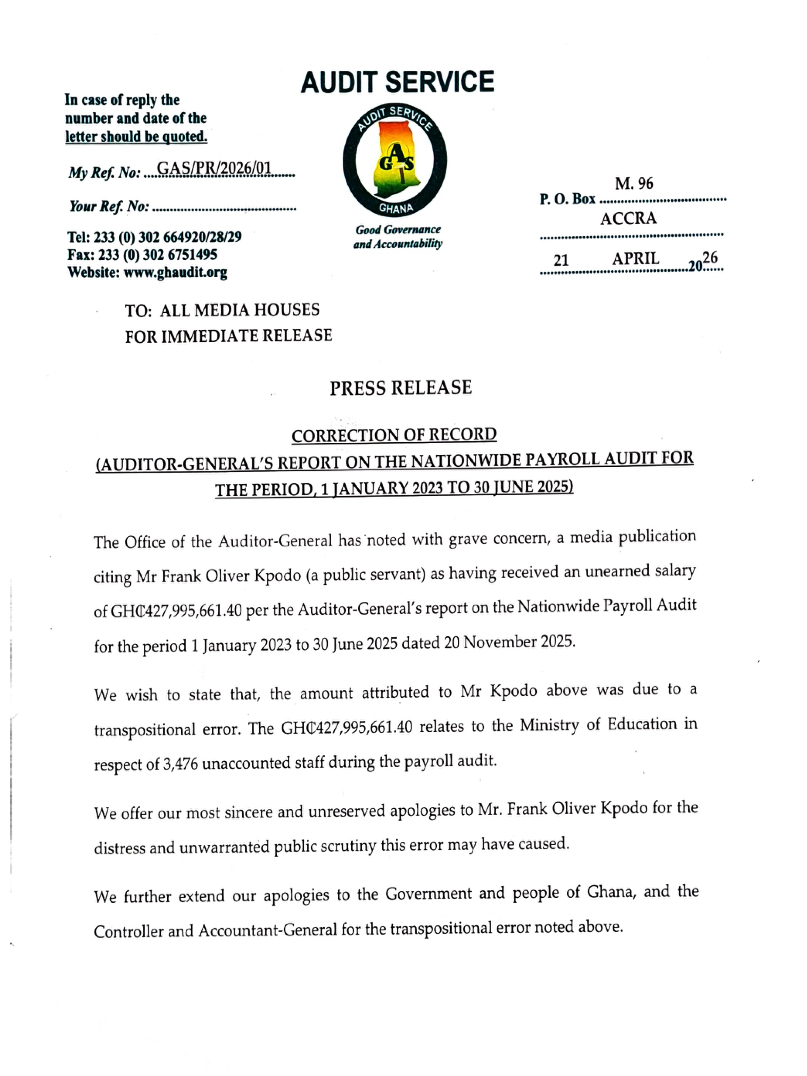

The Ghana Audit Service has retracted an error in its nationwide payroll audit report that wrongly linked public servant Frank Oliver Kpodo to a GH¢427,995,661.40 figure, clarifying that the amount was misattributed due to a transpositional mistake.

In a press release dated April 21, 2026, the Office of the Auditor-General of Ghana acknowledged that a media publication had cited Mr. Kpodo as having received the amount as unearned salary in the Auditor-General’s report covering January 1, 2023 to June 30, 2025. However, the office stressed that the figure does not relate to any individual payment but rather to discrepancies identified during the payroll audit exercise.

According to the statement, the GH¢427 million amount actually pertains to payroll irregularities within the Ministry of Education, specifically involving 3,476 unaccounted-for staff identified during the audit process. The misrepresentation, the Audit Service explained, resulted from a transpositional error in the report.

“We offer our most sincere and unreserved apologies to Mr. Frank Oliver Kpodo for the distress and unwarranted public scrutiny this error may have caused,” the statement said, adding that apologies were also extended to the Government of Ghana and the Controller and Accountant-General’s Department.

The controversy surrounding the GH¢427 million figure had gained traction in sections of the media and on social platforms, with suggestions of large-scale “unearned salaries” within the public sector payroll. However, the Controller and Accountant-General’s Department had earlier rejected such claims, explaining that Ghana’s payroll system has controls that prevent payments beyond approved limits.

The issue forms part of broader concerns over payroll management in Ghana, where periodic audits have uncovered irregularities such as ghost names, unverified staff, and data inconsistencies across public institutions. In recent years, forensic audits particularly within state agencies—have been used to identify and address such anomalies as part of ongoing public financial management reforms.

The Audit Service’s latest clarification is expected to correct public perception and restore confidence in the integrity of the payroll audit findings, while also highlighting the importance of accuracy in reporting sensitive financial data.